FICO 10

Since 2014 The Fair Isaac Corporation (FICO) has calculated your FICO 9 Credit Score. It went into effect in 2014. However, it wasn’t until banks starting using the new score in mass that Fair Isaac made the new formula available to consumers. FICO is the most widely used credit score in the country. 90% of all credit lenders (whether they are selling mortgages, credit cards, personal loans, and more) use the FICO score in some way. Now we have new from Fair Isaac, FICO 10.

FICO 10

We have an upgraded new scoring system from The Fair Isaac Corporation (FICO) called FICO 10, which will incorporate consumers’ debt levels into their scoring model. The new scoring model will also likely create a wider gap between those considered good credit risks and those who are not. Consumers who already have good credit, for example, and who continue to whittle down their already existing loans and make on-time payments will see higher scores. But those who score below 600 will see more significant dips in their scores under the new model.

Consumer advocates have long been pushing to make credit scoring models a snap for people who have debt in collections or medical debt. According to Experian, more than 64 million Americans have some medical collection record on their credit reports. Collection agencies report a whopping 99.4% of medical debts dragging down people’s credit health in the process.

Your credit score now treats medical collections differently than non-medical collections, like credit cards. All in all, your credit score will be less damaged by a medical debt you can’t afford to pay than it would be damaged by, say, that Macy’s card payment you fell behind on.”

What are FICO 10 Credit Scores?

Caroline Mayer, a consumer blogger, says, “It’s an algorithm designed to predict your likelihood of repaying debt. Lenders use your score to determine whether to approve you for loans and credit cards and at what interest rates. Insurers use credit scores to set premium rates, and employers use them when making hiring decisions.

FICO credit scores run from 300, considered the highest risk of default, to 850, the lowest risk. Though FHA for years has accepted applicants who have FICO scores in the 500s, the practical reality has been that most lenders ignore borrowers whose scores are under 620 or even 640.

How are FICO 10 Credit Scores Calculated?

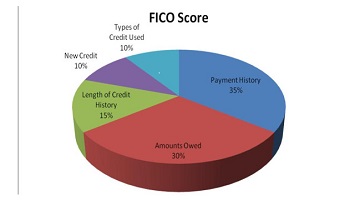

Your score is based on many different pieces of credit data in your credit report here in Kansas City. We don’t yet know the categories in FICO 10 that determine your credit score and the percentages. However, The new models will treat late payments and debt more severely and now consider historical information about your credit card balances and payment amounts. Your FICO® Score will likely change as a result.

If you don’t know your FICO 10 Credit Score, you can request a free copy of your credit report then check it for errors, such as late payments incorrectly listed for any of your accounts and the amounts owed for each of your open accounts. If you find errors on any of your reports, dispute them with the credit bureau. careful with some consumer sites

Careful with Some Consumer Sites

Forbes says to be careful with some consumer sites offering free credit reports. “The new free scores from consumer sites are often “ballparks,” not the ones used by financial institutions to determine credit. Even more confusing, your FICO credit score or Vantage score may differ from lender to lender since each institution can tinker with the parameters.

Some lenders use scores created by FICO. Others use VantageScore, developed by credit rating bureaus Experian, Equifax, and TransUnion. Others compute scores by working with a single credit bureau. FICO and TransUnion’s New Account Score ranges from 300 to 850; Vantage, from 501 to 990; Equifax’s is between 280 and 850, and Experian is 330 to 830.

Got a Low FICO 10 Credit Score?

Making your credit payments on time is one of the most significant contributing factors to your FICO 10 Credit Score. Set up reminders like knotted strings on your fingers for making payments or switch from paying by check to automatic bank debits to each creditor.

Get out of debt. Reducing the amount that you owe will be a far more satisfying achievement than improving your credit score. The first thing you need to do is stop using your credit cards. Yes, you’ll probably use the “gag-me” expression at this recommendation. Come up with a payment plan that pays off the cards. Once you pay off your credit card debt, focus on building an emergency fund equal to six months of living expenses. Finally, save large amounts of money going to interest by paying off your mortgage early.

If you are ready to leap owning a home and have a low FICO 10 Credit Score, shop around. You may get turned down by some lenders because they haven’t reduced their standards yet. Keep shopping until you find one that has. You are likely to find a better reception than you expected.

Ask for FREE information about How to Sell Your House Fast.

Terra Firma Property Solutions, LLC, is a professional, full-service real estate solutions firm.

We buy and sell properties throughout the greater Kansas City area. We specialize in buying distressed homes, then renovating and reselling them to home buyers and landlords. Terra Firma Property Solutions: excited to be part of the economic rejuvenation of Kansas City and its surrounding areas.

Call us today at (816) 866.0566